In the current environment, it’s important for all of us to work smarter and more consciously. That’s why I want to personally update you on the situation with COVID-19 (the coronavirus) and the conscious effort we are making to keep business moving forward while remaining responsible.

2020 has been one of the busiest years in almost two decades for AAR Partners with clients reaching out for agency evaluations and reviews. However, in the recent weeks as the epidemic has rapidly progressed, more and more marketers are either mandated to stop travel or being much more mindful about travel.

New business is our industry’s lifeblood. And with that said, we cannot panic to the point of paralysis. But we can be smart and with that said, use the abundance of technological tools at our disposal to our advantage and curb unnecessary travel for the time being.

With that said, I want to share what AAR Partners is suggesting to clients in order forge forward with the review process but are grounded from flying…

Turn the in-person meetings into a video conference and allow the agencies to craft/control how they would like to conduct the virtual meeting. This will allow them the benefit of exemplifying how adaptable and innovative they are with all sorts of unpredictable situations. It also allows agencies to exhibit how their team thinks innovatively, conducts themselves in a virtual setting and communicates remotely. After all, many meetings regardless of the current situation do take place remotely throughout the year.

With this said, there are a handful of AAR suggestions to help make a video conference or virtual meeting more effective:

1. Connect People: Each team member must be front and center on screen for up to a minute at the start of the meeting. This is to simply introduce him or herself so the client team can identify that person throughout the meeting, get a better sense of him/her and feel more connected when everyone is interacting throughout the session.

2. Online Whiteboard: Use PowerPoint (or whatever program) as a shared background platform in order to keep everyone focused on “on the same page” while discussing open-ended topics.

3. Online Notes: Each agency should have a scribe to capture all vital notes and show those notes on a sidebar discussion forum so everyone is up-to-the-minute in sync with the progress of the remote meeting.

4. Tight Knit Group: Be sure the core team that is responsible for the day-to-day account is front and center on the video session. You can bring in other members but those that have a speaking roll must be in clear sight at all times.

5. Materials in Advance: All materials must be shared 24-hours in advance of the video conference, particularly a detailed agenda. Participants should not be “putting finishing touches” on materials while in the meeting (since they feel that they can’t be seen as they would be in person) instead of actively listening and being involved in the meeting/discussion.

a. Included in these materials should be a 3 minute “spirit of the team/agency culture” video to introduce some of the key team members in advance and give a sense of the agency environment/day in the office.

6. Be Prepared: Both sides must have IT set up and test all connections 30 minutes in advance of the meeting start time in order to avoid losing meeting time in case of connection issues which is a major disruption. Once that happens, everyone’s focus fades quickly.

Virtual meetings do not exactly take the place of an in-person meeting, especially for work sessions and final pitch presentations BUT it is an interesting twist and does allow your team to show the client how you can interact on another level and manage various situations innovatively and effectively.

The best thing we can do as an industry is to continue with business as usual in the face of an unusual situation by using the vast tech tools at our fingertips but adding an element of human touch to it!

AAR Partners is committed to providing all our agency growth partners valuable information you need to make informed decision to help with your new business efforts and agency growth.

We understand travel is fundamental to our business and lives which is why it can’t simply stop. So let’s continue forging forward but for now be conscious about our alternative choices in an effort to protect our industry… and nation.

Pitch with Passion, Lisa

Despite Big Banks’ best efforts, the age of e-banks is accelerating quickly within the banking industry.

A Little History:

Also known as challenger banks, neobanks are branchless, digital-only financial institutions that challenge the traditional banking model.

Challenger banks have their roots in the UK as, during the post-financial crisis in 2008/2009, many financial institutions were consolidated due to financial losses in mortgage defaults and rising interest rates. During this time, banks stopped lending each other money, which meant it was much harder for both consumers and businesses to get credit.

In 2013, in response to the banking crisis, a new opportunity was introduced in the UK. Regulation was changed to allow neobanks to raise capital and build systems before they applied for a full banking license. This gave startups like Starling, the first neobank in the UK, the chance to compete against the bigger, legacy banks.

Since then, other neobanks like Monzo, Atom Bank, Revolut and Tide Bank have entered the UK market, and the neobank trend has gone global, including the United States.

Varo Has Broken into the Vault:

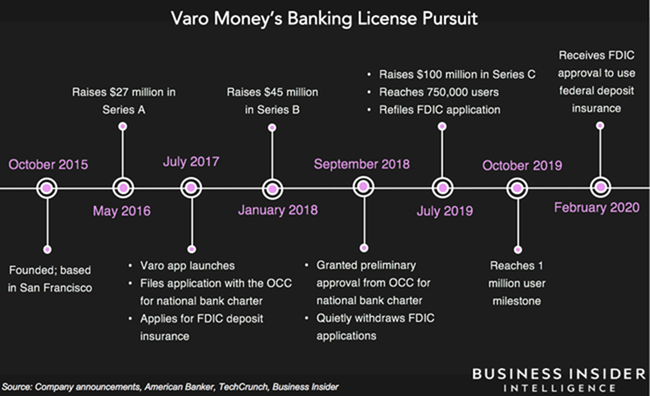

San Francisco-based mobile bank Varo just won approval from the FDIC last week to receive deposit insurance, becoming the first neobank to do so.

For the 5-year-old fintech startup, it’s the first step towards becoming a full-fledged digital bank that can hold cash, give loans, and create credit cards.

The FDIC-approval is a milestone in its three-year journey toward receiving a national bank charter. Upon receiving full bank charter approval, Varo plans to roll out more products, including credit cards and joint accounts.

Although Varo cleared a major hurdle by getting the FDIC’s blessing, it still needs approval from the Office of the Comptroller of the Currency (OCC) and the Federal Reserve.

The startup has already spent 3 years — and ~$100m — getting to the point it’s at today.

Become a Challenger Bank is Challenging:

·huge amounts of red tape.

·regulators prevent fintech companies from taking reckless moves with customers’ money.

·old banks have lobbied aggressively to keep them out of the club.

·fintech startups need banking partners to stay afloat.

Big Banking – Putting Its Mouth Where Its Money Is:

Varo partnered with the Bancorp Bank, but also continued working with federal agencies to find a way to operate independently.

Varo must now clear its final few hurdles to become fully functional.

Meanwhile, Big Banks are using their borrowed time to build out their own online banks to edge out their online rivals.

Goldman Sachs launched its online bank Marcus in 2016. In 2018, Wells Fargo followed up with an app called Greenhouse.

The Opportunity:

Big Banks are on borrowed time and you bank on the fact that it’s only a matter of time before traditional banking is overturned.

Varo may be a neobank to start building a relationship but it has also paved the way for a flood of additional challenger banks coming onto the scene.

Keep a close watch on this sub-category as an opportunity that you can bank on…

Just remember, don’t stalk. Don’t hound. Don’t send a myriad of messages about yourself. So what do you do?

Build trust. Share category insights. Do some light consumer research. Offer purchase pattern eye-openers. Toss out some trends. Show your expertise and how it’s relevant. Just… don’t… sell!

Good luck and remember to prospect smAARt and pitch with passion!

This is an interesting POV written by Seth Godin and applies to our everyday life of pitching new prospects.

The ongoing debate of spec work as part of the pitch process is well, ongoing. The fact is, in many cases “spec work” can be showcased through highly relevant past work creative for past clients with identical or extremely similar marketing issues. Or as Pablo Picasso put it, “I often paint fakes.” Meaning much of his “new” work was a derivative of something prior rather than an original.

Take this insight and apply to new business pitching BUT… the critical component is to exemplify the purpose and relevancy of the work to that prospective client’s specific needs.

I hope you enjoy the quick, insightful and applicable words here written by Seth Godin.

Painting fakes and singing covers

When a pop band goes on the road to promote a hit record, they’re almost certainly re-singing a version of their work that matches what the fan expects to hear, not the daring, original work that they actually might feel like playing that night.

And when, twenty years later, they go on a reunion tour, the same is true, but even more so. The band make-up has changed, their tastes have changed, and they’re an oldies act now. Playing covers of their own work.

Every once in a while, Pablo Picasso painted a daring new work of art. But most of his 10,000 paintings rhymed with the ones he’d done before. In his words, “I often paint fakes*.”

Fakes and covers are an essential element of the creative cultural economy. But when we engage with them, we should do it on purpose and not be confused about what we’re getting (or creating).

*Painting fakes

Ed shares this story with us, via a friend of Pablo Picasso.

I was staying with Picasso in his studio. Every day, dealers would come by to authenticate paintings they were trying to sell… they would ask the painter if the painting was real or a fake.

A dealer came by one day, Picasso glanced at it and without hesitating said, “fake.” Later that day, two more were identified as fakes.

The second day, a different dealer came by. Picasso hardly looked up. “Fake!” he bellowed.

After the dealer left, I couldn’t help myself. “Picasso, why did you say that painting was a fake? I was here, in this studio, last year when I saw you paint it.”

Picasso didn’t hesitate. He turned to me and said, “I often paint fakes.”

Pitch with Passion, Lisa

Compensation Proposals – It’s a struggle that every agency faces when pitching for a new client…

· Are we undercharging?

· Are we overcharging?

· Are we in the right fee zone compared to the competitive agencies?

And on top of it, we all feel pressured to offer more for less. So the answer is to drop your fees. Right?

WRONG!